Different challenges may arise in the process of merging companies, and one of them is the issue of so-called negative equity. We will discuss it using the example of the merger of limited liability companies by way of acquisition from the perspective of Polish law.

What is negative equity?

We talk about the occurrence of so-called negative equity when the company's balance sheet - prepared for the purposes of the merger - shows a negative value for the equity item on the liabilities side. In practice, it may happen that it appears in the balance sheets of both merging companies.

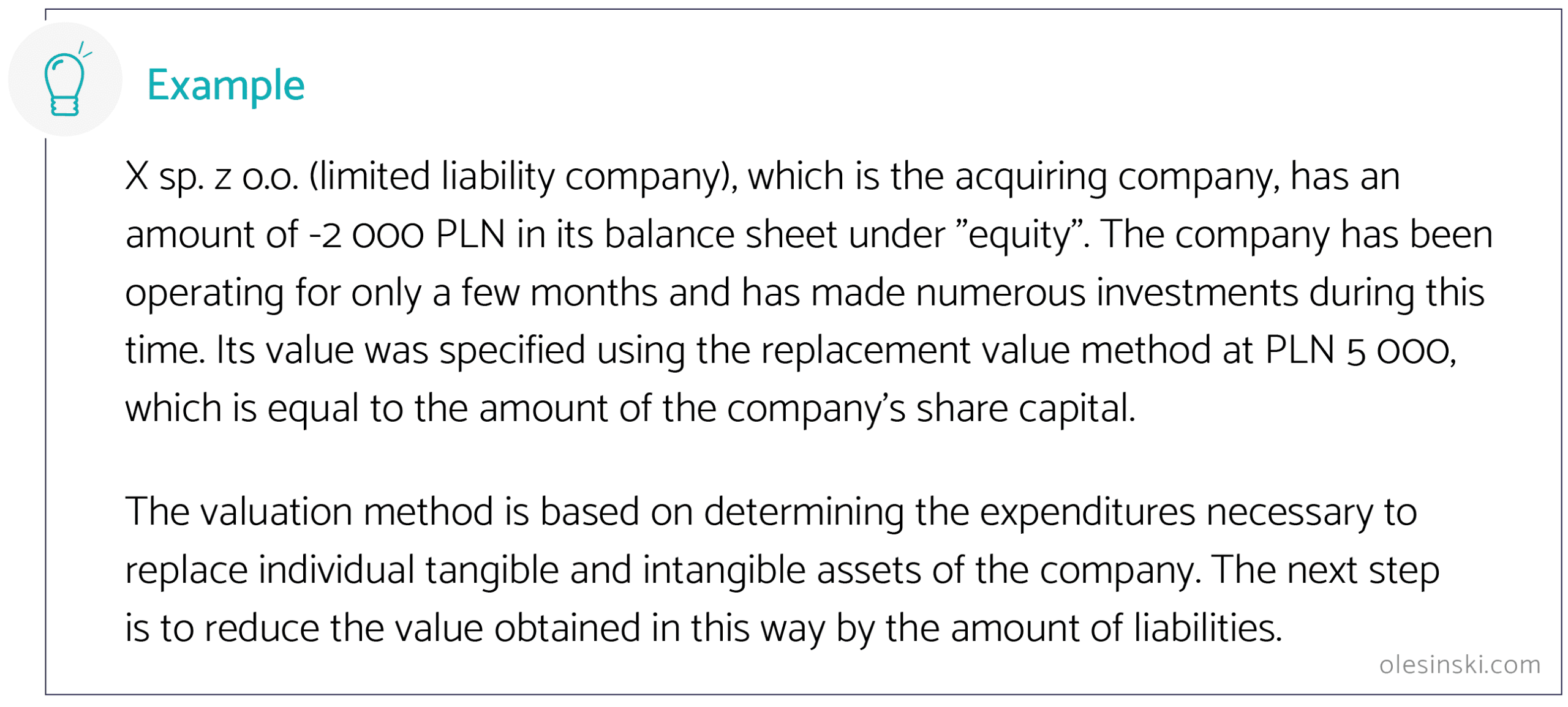

The existence of negative equity does not in itself mean the poor financial condition of the company or, even more so, the need to file a bankruptcy petition. Negative equity may appear, for example, in companies that have recently started their operations and made investments.

Is it possible to merge companies with negative equity?

There are no provisions in the Commercial Companies Code that directly prohibit the merger of companies with negative equity. There is also no dispute in legal doctrine or case law as to the admissibility of mergers involving such companies. On the other hand, we know of individual cases in which courts refused to register a merger when the acquiring company had negative equity.

According to the regulations, the possibility of a merger is not available only to a company in:

- liquidation that has begun the division of assets;

- bankruptcy[1].

The mere existence of negative equity does not prejudge the state of insolvency - possible bankruptcy can only be discussed after the court issues a decision declaring it[2]. Even a company with financial problems can participate in the merger - in practice, the merger may be aimed at restructuring the debt of such a company.

What is important while merging companies with negative equity?

The existence of negative equity may affect the valuation of the company's assets, which affects the determination of the share exchange parity.

Therefore, in the case of a merger of a company with negative equity, the method of valuation of assets will also be important. It may turn out that when choosing an appropriate valuation method, despite negative equity, the value of the company's assets will be positive.

If the values of the assets of both merging companies are positive, determining the share exchange parity should not be difficult. However, doubts may arise when the value of the company's assets resulting from the valuation turns out to be negative or zero. In such a case, determining the parity taking into account the usually applied principles may be impossible. In such a situation, it is permissible to determine the parity in a conventional manner.

The issue of determining the share exchange parity is very important for the shareholders of merging companies. The parity directly affects their situation in the acquiring company and has a real impact on the "balance of power" in the organization after the merger.

For this reason, it is important to analyze the issue of negative equity, choose the best valuation method for specifying the value of the company's assets and pick the method for determining the share exchange parity.

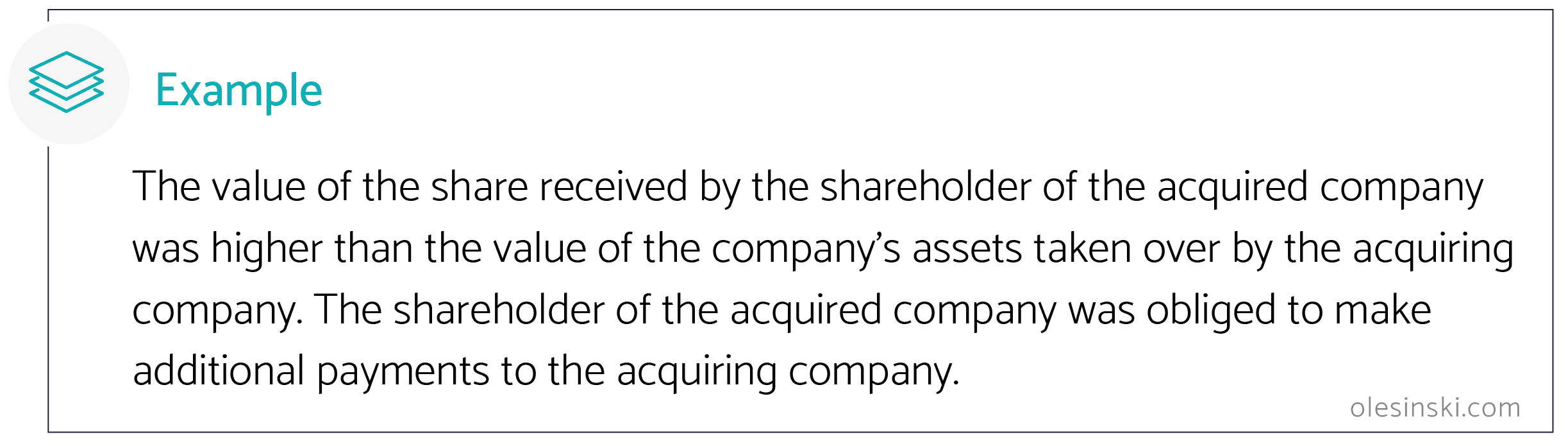

Regardless, any inequalities in the value of assets contributed to the company and the shares received can be equalized through additional payments.

How does negative equity affect the merger of companies in practice?

Courts usually don’t question the possibility of merging companies with negative equity - although different approaches do occur (but they are rare). However, each case requires an individual assessment, and appropriate preparation for the merger process – including the selection of a method for valuing assets. If you need support in this area or have any questions regarding the discussed issue, feel free to contact us!

[1]Article 491 § 3 of the Commercial Companies Code

[2] The conditions for insolvency are specified in Article 11 of the Bankruptcy Law.